Why 40% of AI Projects Will Fail While Africa Builds Real Infrastructure

Welcome back to Data Under Glass, where we surface the patterns your pitch decks ignore and the risks your models can’t see.

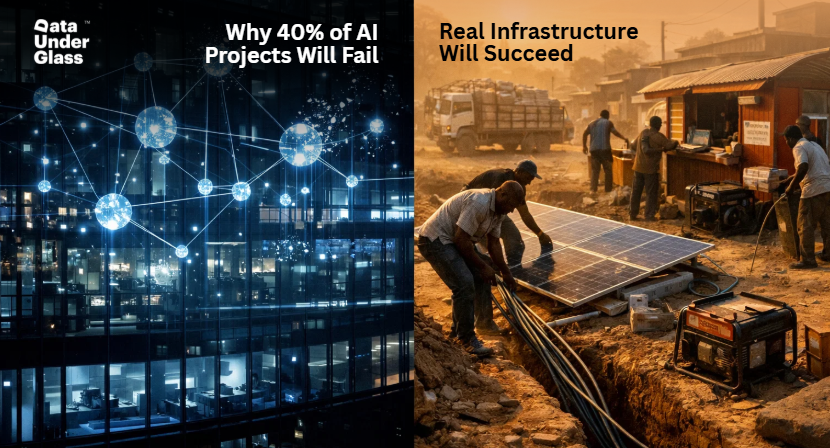

Two stories defined the final quarter of 2025.

In North America, 40% of enterprise applications are racing toward agentic integration by the end of 2026. Billions are flowing into systems designed to plan, execute, and optimize without human oversight. The promise: infinite scale with zero headcount.

In Africa, startups raised over $3.5 billion in 2025, a 59% surge that ended the two-year funding winter. But the narrative has shifted; it’s no longer about “disruption” but about infrastructure that works when everything else fails.

While one market is betting on intelligence, the other is betting on utility.

By mid-2026, we’ll know which bet was built on sand.

— Anderson Oz’.

Case In Point: B2B SaaS, Series A, North America

Raised: $12M

The Pitch: Deploy AI agents to automate customer success workflows. Three-month pilot showed 40% reduction in support tickets and the board loved the metrics. Full rollout budget approved: $4.2M for agent infrastructure, $2.8M in engineering hours.

What We Caught: The agents worked, technically. They answered questions, routed tickets, closed simple cases. Support volume dropped exactly as projected.

But we ran the numbers underneath the numbers.

Customer satisfaction fell 18% and churn climbed 12%. Users weren’t getting better service. They were getting trapped in automated loops that deflected problems instead of solving them.

The metric looked good but the business was walking dead.

The Reality: 39% of organizations are experimenting with agents, but only 23% have successfully scaled them beyond a single business function. The gap between pilot and production isn’t technical. It’s operational.

Most agents are rebranded chatbots; they route, they respond but don’t reason. And customers can tell the difference within 30 seconds.

The Intervention: We ran a two-week reality audit, interviewed 40 customers. Analyzed 2,000+ support interactions. The truth was brutal: customers didn’t want faster ticket resolution. What they wanted was products that didn’t break.

The fix wasn’t better agents but better software.

We reallocated the $4.2M agent budget to product stability. Customer satisfaction recovered within 90 days. Support volume dropped 31%, not through deflection, but through prevention.

The Lesson: Gartner predicts that over 40% of agentic AI projects will be canceled by the end of 2027 due to escalating costs, unclear business value, and what they’re now calling “agent-washing”, rebranding basic automation as autonomous intelligence.

Agents aren’t the problem but building them to hide broken products is.

North America’s Bet: The Leap of Faith

The thesis sounds perfect: automate multi-stage workflows, build the human-less startup, scale infinitely with minimal headcount. 57% of organizations now deploy agents for cross-functional processes spanning multiple teams.

In 2026, we’ll see organizations that employ more AI agents than humans. Small teams doing the work of hundreds. Software writing itself and customer support running 24/7 with zero human cost.

Until the model changes, the API goes down and a customer asks something the agent wasn’t trained for.

The Cracks:

Africa’s Bet: The Utility Multiplier

Africa isn’t racing to automate. It’s racing to electrify, connect, and transact.

VCs pivoted hard in 2025. Out: consumer apps burning through runway. In: payment rails, mobility networks, clean energy infrastructure, B2B SaaS with recurring revenue.

The numbers tell the story: clean energy surpassed fintech as the top-funded sector by Q3 2025, securing 53% of all investments, nearly $950 million. Kenya alone captured 57% of Q3 clean energy funding at $560.9 million.

But here’s the real signal: venture debt surpassed equity for the first time in 2025, representing 45% of total funding. This isn’t a symptom of funding winter. It’s a maturation signal.

Banks and development finance institutions are lending against cash flows, not potential. When debt markets open up, it means investors see real revenue, real customers, and real unit economics.

Africa isn’t ignoring AI, it’s refusing to automate poverty.

While North American founders chase “agentic ROI,” Moniepoint became Africa’s first profitable fintech unicorn in October 2025.

The Numbers:

The Strategy:

Moniepoint didn’t build a pure-play digital bank. They built a hybrid infrastructure: digital wallets backed by 2 million physical agents operating out of shops, markets, and kiosks across Nigeria.

When the internet goes down, transactions don’t stop. When power fails, the network keeps moving. The technology is sophisticated, but it’s wrapped in analog resilience.

This wasn’t idealism, it was necessity.

Currency volatility in Nigeria, Kenya, and Egypt forced entrepreneurs to build FX-resilient models that generate revenue in local currency but protect value across borders. Payment infrastructure that works on USSD, not just apps. Business models that survive 40% devaluations.

In North America, profitability is finally becoming non-negotiable. In Africa, it was never optional.

1. Infrastructure Over Intelligence

The winners solve problems first, then automate solutions.

Kenya’s clean energy boom didn’t start with AI optimization models. It started with solar securitization, bundling distributed energy contracts into investable assets that banks could lend against.

Solar panels work when the grid fails, AI agents don’t.

2. The USSD-Plus Resilience Model

If your product requires 5G to function, it’s culturally irrelevant in 60% of the world.

One payments company we advised had a beautiful mobile app. Rural Kenya conversion: 4%. After adding USSD fallback that worked on any phone, any network, one bar of signal: 31% conversion.

Culture isn’t language, it’s constraint. Build for the infrastructure reality, not the infrastructure aspiration.

3. Trust Migration: Human-to-Digital Handshakes

Pure digital flows failed across South Africa’s financial sector in 2025. Hybrid models won.

One retail fintech tried mobile-only lending. Approval rate: 38%. They added human verification at partner locations for first-time borrowers, then migrated users to fully digital flows.

Approval rate jumped to 67%. Default rates dropped 23%.

Trust doesn’t digitize at 1:1 parity, it migrates gradually. The companies that respected this reality outperformed those that didn’t by 4.7x.

You may also enjoy reading: The Infrastructure Arbitrage: Building Where Others Can’t (Or Won’t)

Before you deploy another agent, run these four stress tests:

1. The Deflection Check

Does this agent solve the customer’s problem or just stop them from talking to us? If CSAT drops while ticket volume falls, you’re deflecting, not delivering.

2. The One-Bar Performance Test

Can this workflow survive on 3G with intermittent connectivity? If not, you’re building for aspiration, not reality. Over 60% of the world still operates on constrained infrastructure.

3. The Securitization Test

Could you raise debt against this workflow? If a bank won’t lend against your “automated revenue,” your unit economics are fantasy. Real businesses generate cash flows banks trust.

4. The Infrastructure-First Filter

If the AI model costs 10× more tomorrow, is the underlying service still valuable? If the answer is no, you’re renting capability, not building equity.

✓ $3.5B raised by African startups in 2025, up 59% YoY

✓ 40% of enterprise apps will include AI agents by end of 2026

✓ 40% of agentic AI projects will be canceled by 2027 due to costs and unclear value

✓ $950M in cleantech funding by September 2025, surpassing fintech

✓ 45% debt financing in Africa 2025, first time exceeding equity

✓ 57% of orgs deploy multi-step agent workflows

✓ Signal: Profitability beats automation. Infrastructure outlasts intelligence.

✓ Noise: Agent-washing, growth without revenue, automation without purpose.

Agents are tools. Infrastructure is strategy.

North America is automating everything. Africa is building what works when everything else fails.

The companies still standing in 18 months won’t be the ones who deployed agents fastest. They’ll be the ones who understood that technology serves people—not the other way around.

Before you invest another dollar in agentic AI, ask yourself: Are you solving a problem, or are you automating a fantasy?

Data Under Glass is an exclusive weekly deep-dive analysis uncovering the data-driven stories behind the most successful scale-ups. We surface the patterns your pitch deck doesn’t capture and the risks your Excel model can’t see.

Forward this to the founder who thinks more agents equals more value.

Till next time, this insight is DUG Weekly!